by Peter Schiff, Schiff Gold:

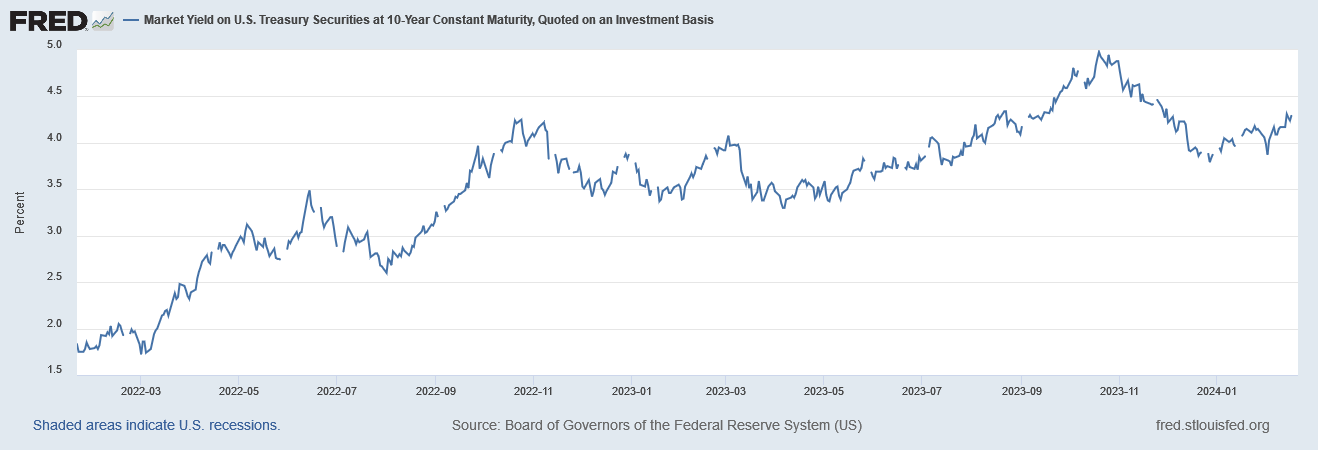

The gold price has been surging, with unprecedented central bank demand gobbling up supply. It has been a force to behold — especially as US monetary policy has been relatively tight since 2022, and 10-year Treasury yields have rocketed up, which generally puts firm downward pressure on gold against USD.

The gold price has been surging, with unprecedented central bank demand gobbling up supply. It has been a force to behold — especially as US monetary policy has been relatively tight since 2022, and 10-year Treasury yields have rocketed up, which generally puts firm downward pressure on gold against USD.

TRUTH LIVES on at https://sgtreport.tv/

US 10-Year Treasury Yields Since March 2022

The golden bull has undoubtedly been fueled by an unstable US election year, inflation worries, expectations of rate cuts later in 2024, and wars in Ukraine and, more recently, the Middle East. But there’s another secret sauce on top of gold’s rise: a weak Yen fueling a rush to inflation-resistant safe haven assets in Japan.

Stunning 1-Year Increase in Gold vs Yen

Source: TradingView.com

When gold and VIX (a volatility index) are up, it’s a measure of increasing uncertainty in global markets. The Yen often follows, as investors see it as a more stable option compared to the currencies of many other economies. The Yen is also popular for carry trades, where investors look for a currency (like the Yen) that they can borrow at a low-interest rate to invest in assets with higher yields, boosting the Yen in global markets when investors pay back the loans.

But the Bank of Japan has maintained a zero (ZIRP) or negative interest rate policy for the better part of a decade, and now, most economists expect ZIRP to end at the central bank’s next major policy meeting in April. Sustained low-interest rates haven’t stopped Japan from entering a recession, but the expectation is growing that an intervention in the other direction will be needed to shore up the Yen, leading to a potential price trend reversal against gold and other assets.

Gold’s Journey Up Against the Yen Amid Years of Zero Interest-Rate Policy (ZIRP)

Source: TradingView.com

If this reduces demand for gold in Japan, it could cause the yellow metal to drop against the Yen and dampen the fury of the current bull market. But with Japan’s economy addicted to such low interest rates, and few central bank policy tools to meaningfully fix the problem, it’s far from certain that what the BoJ does can possibly be enough to save Yen from continuing its slow-motion collapse.

Besides, while a change from ZIRP in Japan would be a big change, the BoJ has made it clear that any shifts would still maintain a relatively accommodative monetary policy. With rates ultra-low for so long, upticks would have to be careful and gradual. As quoted by Reuters late last year, Daiwa Securities’ Mari Iwashita said:

“Even with the lifting of the negative rate policy, the BOJ will explain that the financial environment is still accommodative.”

Japan is an interesting case because of sustained ultra-loose policy even as other countries, like the US, have more recently undergone rate hikes to prevent runaway inflation. Many central banks are expected to loosen policy again later this year just as Japan appears poised to do the opposite, potentially maintaining demand for gold, but shifting it from Japan to other countries where interest rates will be going down again.

However, with the Fed recognizing it has backed itself into a corner with its policies, it is now considering tightening in some ways and loosening in others — so it’s hard to tell for sure what effects this central bank contradiction chaos will have on the price of gold. But it will be interesting to see exactly how much the BoJ tightens, and whether investors become convinced that any resulting increases in the Yen’s strength will be based on a solid foundation.

With the post-COVID stimulus inflation genie still not back in the bottle in the US, rate cuts will only make the problem worse, and market confusion from such double-edged “solutions” might just lead to more flight to safety in the form of gold. Even if the Yen strengthens somewhat, we’ll see a generally weaker dollar in 2024 — and continuing bullish demand for the ultimate safe haven asset.