by Wolf Richter, Wolf Street:

![]() Huge profits in subprime caused specialized dealers/lenders to take big risks, which came home to roost. But prime auto loans are in pristine shape.

Huge profits in subprime caused specialized dealers/lenders to take big risks, which came home to roost. But prime auto loans are in pristine shape.

Subprime doesn’t mean “low income,” it means “bad credit”; it means a history of taking on too much debt and not paying those debts and other obligations as agreed, which caused their FICO score to drop into the subprime category.

TRUTH LIVES on at https://sgtreport.tv/

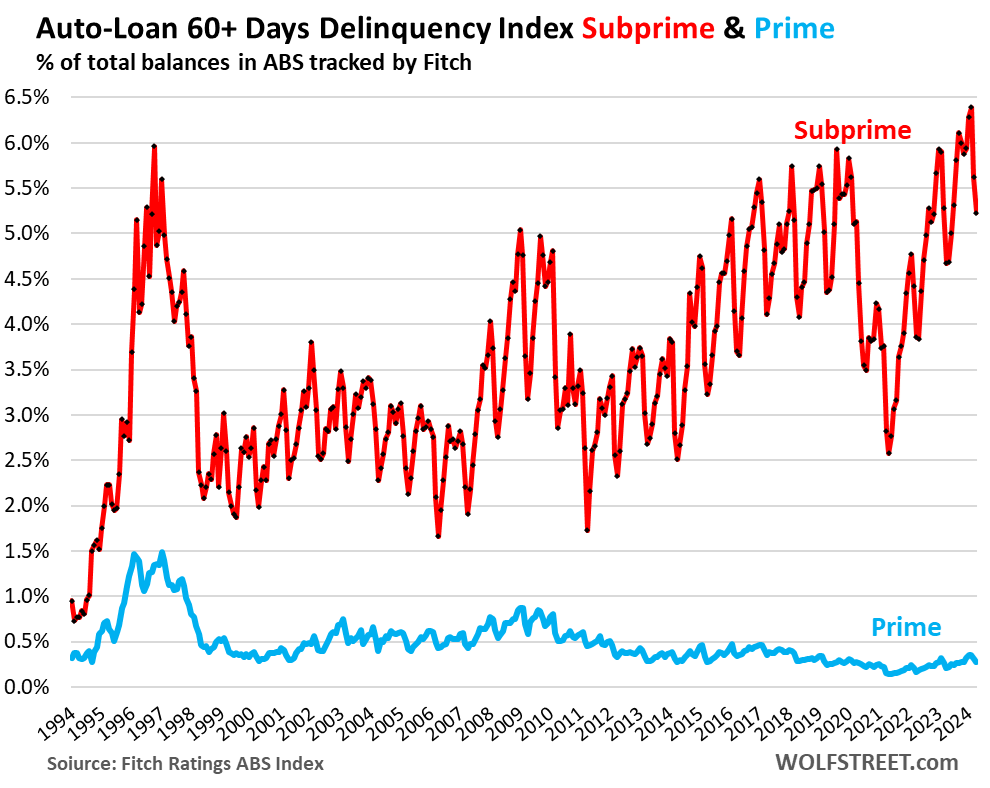

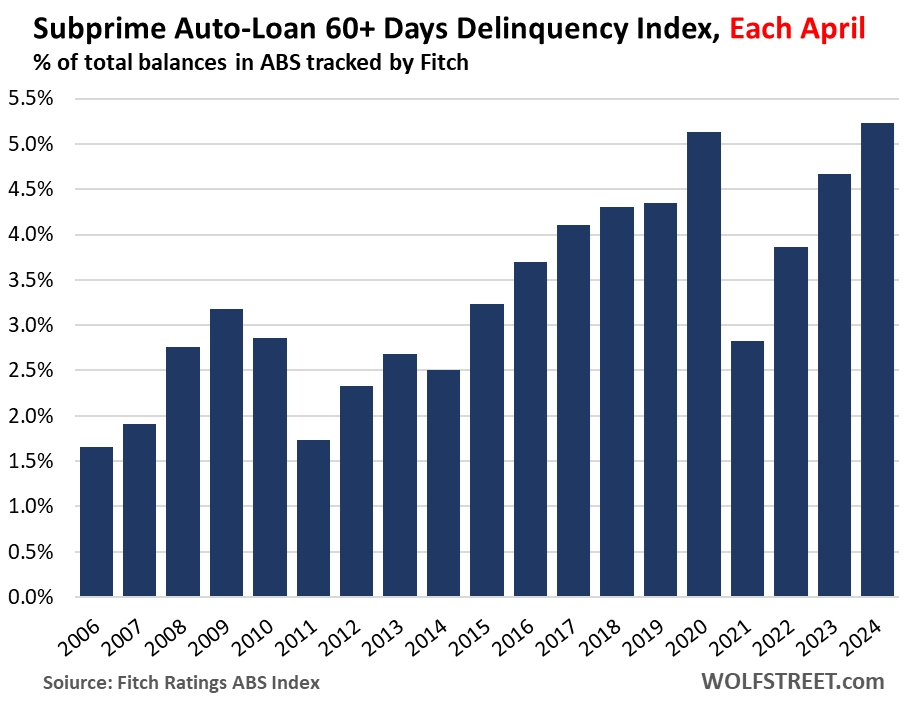

And subprime auto loans are getting into trouble, after the free-month era got them temporarily out of trouble. In April, 5.23% of subprime auto loans were 60 days or more delinquent, the worst April on record, and a hair above the prior record of April 2020, according to the Fitch subprime index, which tracks auto loans that have been securitized into the asset-backed securities (ABS) that are rated by Fitch.

The index is seasonal, with highs every January or February and lows in April or May, as tax-refund season bails out many a borrower. February 2024 had been the highest of any month on record with a delinquency rate of 6.4% (red). But prime auto loans are in pristine conditions (blue).

The Aprils of every year going back to 2006.

You can see that subprime delinquencies were already rising from 2025 through 2019, as subprime lending was getting very aggressive, leading to a slew of scandals, big losses, and the collapse of some PE-firm-owned specialized subprime dealer/lenders in 2018, some of which we discussed at the time, so we’re kind of used to the subprime drama and take it in stride.

The thing is, subprime is a business with huge profit margin on selling the cars, and huge profits on financing the cars at dizzying interest rates, and so specialized companies take big risks to get to those profits, and for some, it ends in a collapse when the risks come home to roost.

Subprime is only a small part of used vehicles, doesn’t impact new vehicles.

With auto loans, nearly all subprime lending is for used vehicles, and most of it is for older used vehicles. The sweet spot is around 10 years old. It’s very difficult to finance a new vehicle with a subprime credit score.

About 61% of used vehicle buyers pay cash, according to Experian. For the 39% who borrow to buy a vehicle, the share of subprime borrowers was about 14% of loan originations. This means that about 5.5% of all used vehicle buyers (those that pay cash and those that finance) get subprime loans. It’s just a small specialized high-risk high-profit corner of the overall used vehicle market.

The subprime share used to be higher before the pandemic, a sign that subprime lending has tightened in 2023, as it always does when delinquencies pile up.

Prices and the mess.

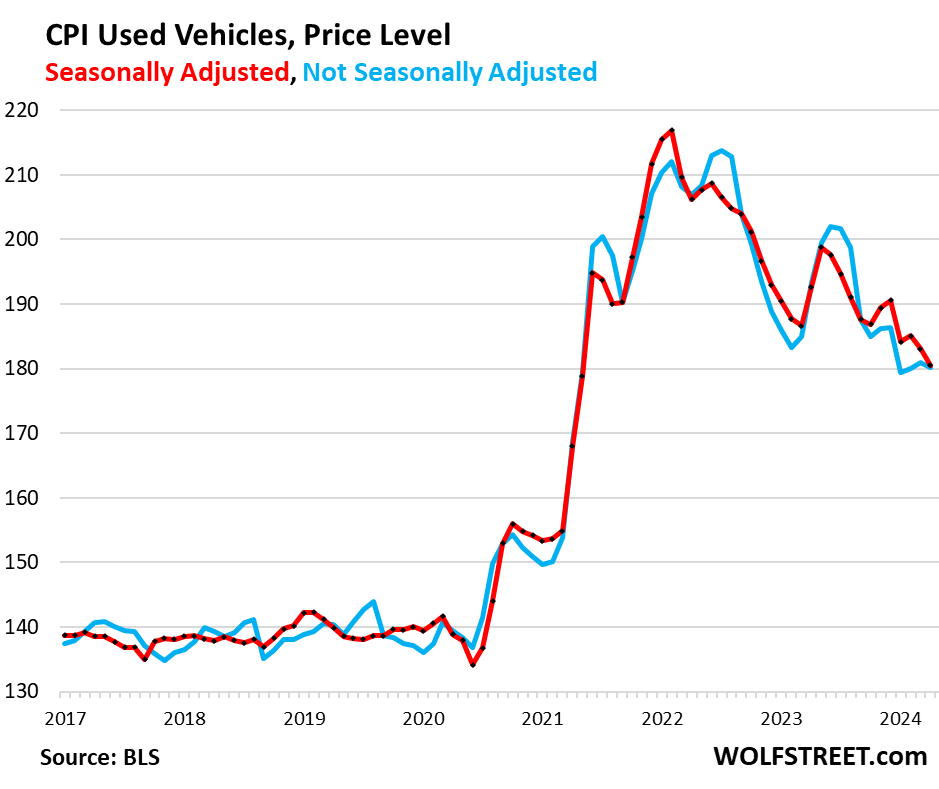

But used vehicle prices spiked by about 55% in 2020 through 2021, and people took out big loans to finance these massively overpriced used vehicles. Since early 2022, used-vehicle prices have given up nearly half that spike, but they’re still very high, and interest rates have shot up. These movements have turned the used-car business upside down.

A few PE-firm owned specialized subprime dealers/lender chains collapsed in 2023, and the largest publicly traded subprime dealer/lender Car-Mart disclosed big problems, and its stock tanked nearly 50% since mid-August, despite the booming stock market.

Losses for investors have been less severe.

The subprime business hinges on the dealer/lender being able to securitize the subprime auto loans into Asset Backed Securities (ABS) and sell the investment-grade tranches of those ABS to pension funds and other yield-seeking institutional investors, and sell the riskier junk-rated tranches that take the first losses to investors seeking higher yields.