by Pam Martens and Russ Martens, Wall St On Parade:

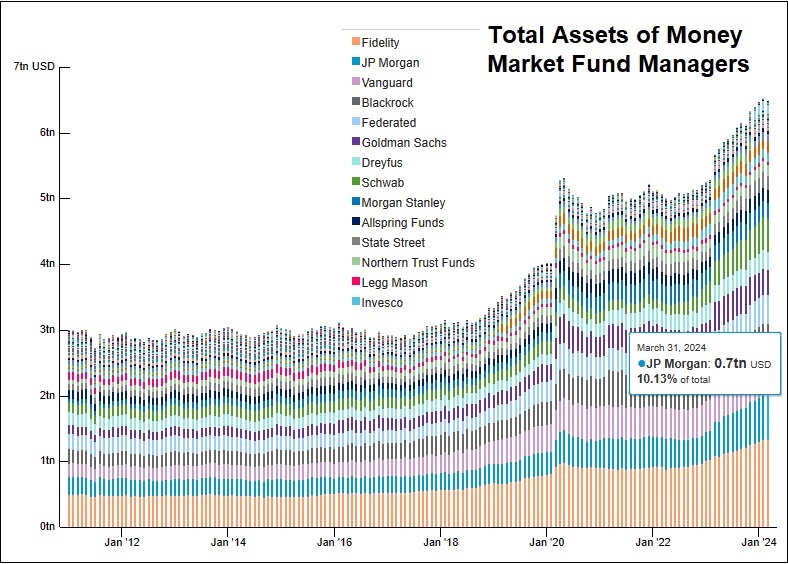

The Office of Financial Research (OFR), the federal agency created after the financial crash of 2008 to keep federal banking regulators on top of threats to financial stability, has posted an interactive chart showing the largest managers of Money Market Mutual Funds in the U.S. Alarmingly, the parent of the largest and riskiest bank in the United States – JPMorgan Chase – is also the second largest Money Market Mutual Fund manager.

According to the OFR, as of March 31, 2024, JPMorgan was managing $657.9 billion in money market funds, second only to Fidelity, which on the same date was managing $1.3 trillion in money market funds. The data comes from Securities and Exchange Commission Form N-MFP2.

TRUTH LIVES on at https://sgtreport.tv/

JPMorgan’s federal regulators have failed to stem the bank’s growth despite the fact that JPMorgan Chase has been tapping massive bailouts from the Federal Reserve since the last quarter of 2019, as well as being charged with nonstop crimes.

During the COVID-19 pandemic in 2020, the Fed created an alphabet soup of emergency lending programs, one of which was the Money Market Mutual Fund Liquidity Facility (MMLF). When the Fed finally released the granular details two years later of which firms tapped the emergency facilities, it showed that 10 of JPMorgan’s money market funds needed to borrow a combined $8.97 billion on the MMLF’s very first day of operation. The $8.97 billion represented 32 percent of the $27.15 billion in funds loaned that day by the Fed’s MMLF.

JPMorgan money market funds’ liquidity problem on March 23, 2020 appears to have centered on JPMorgan’s tax-free money market funds holding billions of dollars in New York City’s Metropolitan Transportation Authority’s (MTA’s) short-term revenue notes. Those were prominent among the instruments submitted as collateral to the Fed for loans from the MMLF. The MTA notes apparently could not be sold by JPMorgan to meet redemption requests without causing the money market fund to break the buck. Money market mutual funds are expected to trade at a stable $1.00 per share. It is known as “breaking the buck” when money market funds trade for less than $1.00 per share. Breaking the buck occurred at several money market funds during the financial crisis of 2008 and increased the financial panic occurring at the time. To stem the run on money markets in 2008, the U.S. Treasury was forced to take the unprecedented step of guaranteeing money market mutual funds.

Why JPMorgan’s money market funds had such concentrated exposure to one municipal issuer’s notes should warrant the attention of its regulators.

JPMorgan was also an outsized user of the Fed’s Primary Dealer Credit Facility. The transaction data released by the Fed showed that at the end of the first 11 business days of operation of the PDCF, on April 3, 2020, the Fed had an outstanding balance in the PDCF of $49.5 billion and the trading unit of JPMorgan had borrowed $14 billion of that, or 28 percent of the total.

JPMorgan’s need to tap the emergency repo loans from the Fed, which began on September 17, 2019 – months before there were any reported cases of COVID-19 anywhere in the world – was also deeply alarming. According to the quarterly data releases by the Fed for its emergency repo loans (after a delay of two years), the trading unit of JPMorgan (J.P. Morgan Securities) borrowed $2.59 trillion in term-adjusted cumulative repo loans in the fourth quarter of 2019 (see chart below) and another $3.6 trillion in the first quarter of 2020.

Read More @ WallStOnParade.com