by Pam Martens and Russ Martens, Wall St On Parade:

It took eight years of research to compile a data set of annual balance sheets of more than 11,000 commercial banks dating back to 1870 in 17 advanced economies. And in every country, the study arrived at the same finding: concentrating the banking system in the hands of five or less giant banks leads to financial instability and more severe financial crises. The bank balance sheets of the following countries were examined: Australia, Belgium, Canada, Denmark, Finland, France, Germany, Italy, Japan, Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, the United Kingdom, and the United States.

TRUTH LIVES on at https://sgtreport.tv/

The 150-year banking study is titled: “Survival of the Biggest: Large Banks and Financial Crises.” Its authors are Matthew Baron of Cornell University; Moritz Schularick of the Kiel Institute for the World Economy and Sciences; and Kaspar Zimmermann of the Leibniz Institute for Financial Research SAFE.

Other key findings from the study include the following:

“First, we find that large banks are substantially less likely to fail in banking crises than smaller banks. Smaller banks also tend to be absorbed at high rates by large banks in the aftermath of crises. As a consequence, the market share of large banks tends to grow in crises, making them even more dominant going forward. We call this repeated pattern during crises the ‘survival of the biggest.’ We show that the aftermath of banking crises can account for 40% of the total increase in top-5 banks’ asset share across history.”

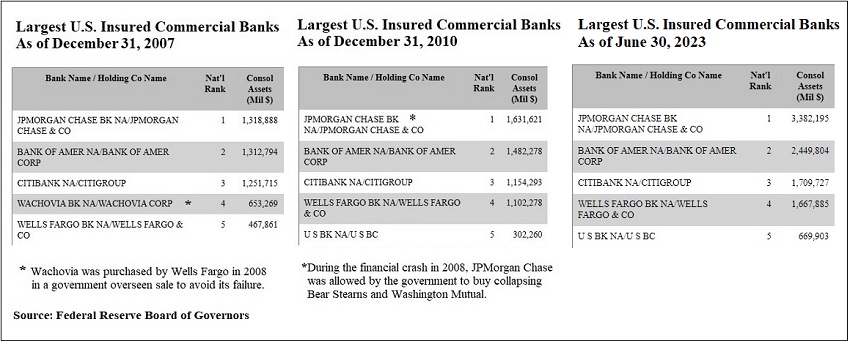

Let’s pause here for a moment and examine that finding in relation to what happened during the financial crisis of 2008 in the United States and this past spring. The largest bank holding company by assets in 2008 was JPMorgan Chase. During the 2008 crisis, federal regulators allowed JPMorgan Chase to buy Bear Stearns and Washington Mutual as they collapsed. JPMorgan Chase went on to admit to an unprecedented five felony counts brought by the U.S. Department of Justice between 2014 and 2020 and developed a rap sheet rivaling an organized crime family; but that didn’t stop its federal regulators from handing it First Republic Bank and its approximately $200 billion in assets after First Republic failed this past spring. As our chart below shows, JPMorgan Chase has more than doubled in size since 2010 to $3.38 trillion in assets as of June 30. Bank of America has grown by almost $1 trillion in assets since 2010. Wells Fargo has grown by $1.2 trillion since the financial crisis.

Despite mega banks in the U.S. creating the worst financial collapse since the Great Depression in 2008, federal regulators handed the same problem banks more assets during the 2008 financial crises. (Bank of America was allowed to buy Merrill Lynch during the financial crisis in 2008 and Wells Fargo was allowed to buy Wachovia Bank during the crisis.)

Another key finding from the new study also buttresses the findings of the Financial Crisis Inquiry Commission following the financial collapse of 2008 in the U.S. The authors write:

“One may ask whether ‘survival of the biggest’ is due to more prudent behavior of the large banks in the run-up to crises. Our second finding is that the opposite is true. Large banks typically take more, not less, risk than smaller banks in the run-up to crises, and large banks suffer bigger equity losses and contract their lending more in the aftermath of crises.”

So why would federal regulators allow these imprudent banking behemoths to grow even larger during a crisis? The authors write:

“…We show two (potentially interconnected) results: first, policymakers are substantially more likely to rescue top-5 banks on the verge of failure, and, second, large banks have more stable funding dynamics in crises, despite greater equity losses. To show the first of these results, we systematically examine top-20 banks across all historical banking crises and create a database of government rescues at the individual bank level—specifically, for all banks that exit or have stock returns less than -90% (which we interpret as being ‘on the verge of failure’). We find that, among banks ‘on the verge of failure,’ interventions explicitly intended to prevent failure and preserve the original banking institution are very common for top-5 banks but a lot less common for banks 6-20 (which instead tend to be merged away or wound down).”

In the U.S. since 2008, the Federal Reserve Bank of New York has become the perpetual money spigot to the reckless banking behemoths. Despite having no elected officials, the New York Fed is allowed to create money electronically out of thin air to shore up the mega banks’ balance sheets when their reckless trading activities require mending.

Read More @ WallStOnParade.com