by Alasdair Macleod, GoldMoney:

This article points to the factors driving sterling gilt yields higher. They are likely to lead to a sterling crisis as foreign selling gathers pace of gilts acquired since 2018. Before interest rates began to rise, foreign buyers had enjoyed higher gilt prices which more than offset losses on sterling. That is no longer the case.

Instead, there is growing disaffection with the Bank of England’s performance and perhaps a realisation that a general election in only 18 months’ time introduces political risk.

TRUTH LIVES on at https://sgtreport.tv/

This article explains the consequences of denying Say’s law, otherwise known as the law of the markets, and by pursuing interest rate policies which have been disproved as a means of controlling inflation. Furthermore, it will be increasing shortages of bank credit which drive interest rates and bond yields higher, not central bank policies.

These are factors which affect all currencies allied to the dollar. The difference between the dollar and sterling is not so much to be found in broad policy dissimilarities, but the lower levels of foreign confidence in sterling as a currency in uncertain times.

Introduction

Of the four major western alliance currencies, only one shares its underlying economic characteristics with one of the others. In this respect, sterling is the poor man’s dollar. While financial headlines have focused on the dollar, sterling has been side-lined. But this is now changing.

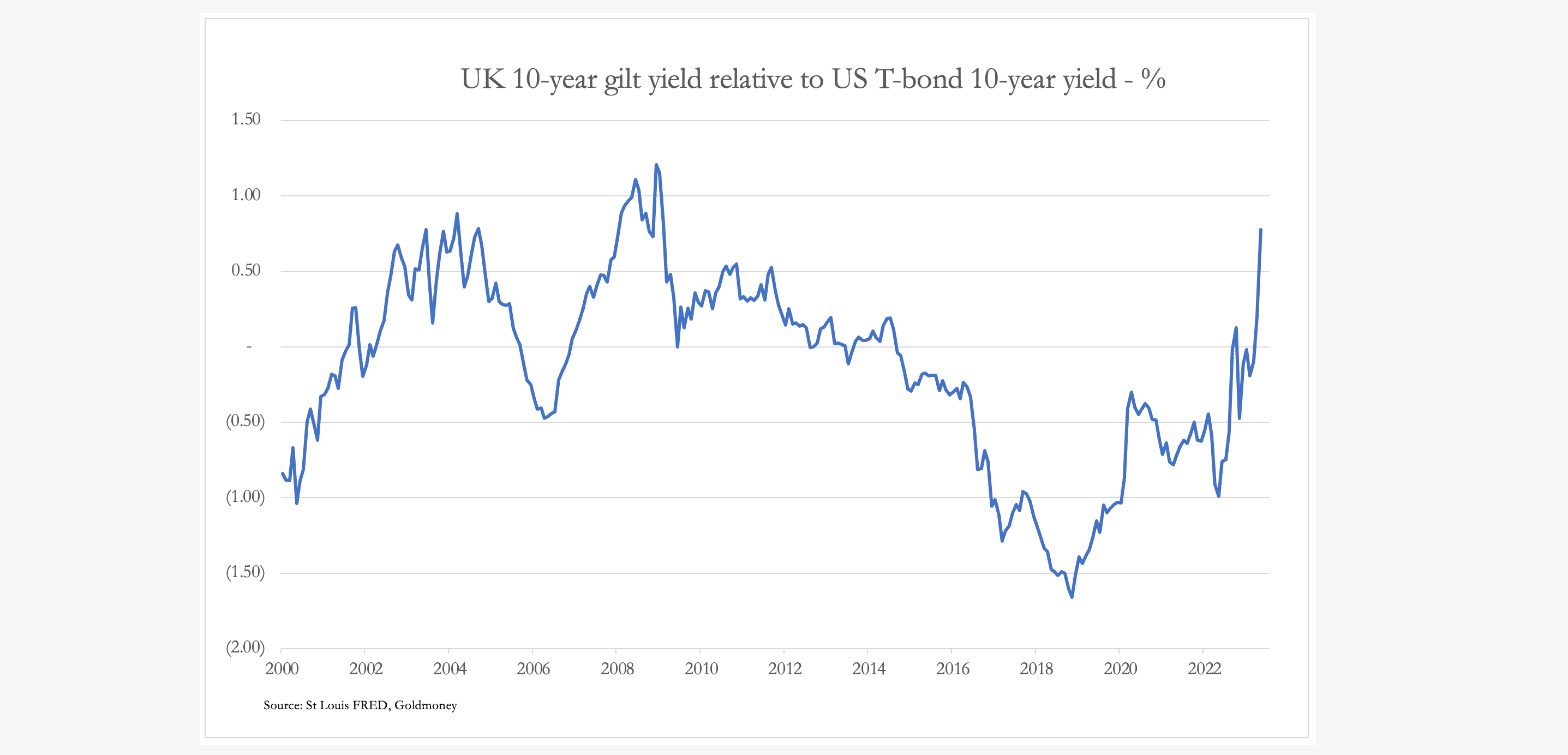

After a period when the 10-year UK gilt yield was significantly less than that of the equivalent US Treasury bond, the former’s yield is now racing ahead as the chart below shows.

It is worth observing that the sudden increase in the gilt yield takes it back to similar levels when the market reacted badly at the time of the Truss administration’s budget, the reaction to which created a crisis for pension funds forcing them to liquidate gilts at any cost to meet margin calls. The return of gilt yields to those levels is therefore a warning not to be ignored. But instead of UK pension funds in crisis, we must turn our attention to international investors, thought to have invested about £200bn in gilts since 2018, but already turning net sellers if the rise in yields is anything to go by.

This loss of foreign appetite for gilts in currently echoed in US Treasuries. Conventionally, global investors regard US Treasury bonds as the risk-free investment against which all others are measured relatively by yield premiums. But that only really applies at times of crisis when a combination of yield and currency relative to the dollar together reflect a flight to safety. At other times, individual central bank interest rate policies can dominate bond pricing.

To complete the comparison between bond yields in the UK and the US we must therefore look at changes in the sterling/dollar exchange rate as well. This is our next chart.

Before the last combined banking and financial crisis in 2008, sterling had rallied strongly against the dollar. When the crisis struck, sterling lost all gains made since the year 2000 when it peaked at over $2.000, taking it back to $1.4000. Now that we appear to be in the early stages of another US banking and financial crisis, a question over the future course of sterling arises in potentially similar conditions.

Until covid struck in 2020, international holders of sterling and sterling securities had patiently absorbed a combination of lower bond yields and gently declining currency values relative to the US “risk-free” alternative. Since then, while sterling has continued to decline, the yield discount on gilts relative to US Treasuries began to narrow, and since January this year has turned into a sharply rising premium. The least one can say about this turn of events is that whatever reasons foreign holders of gilts had for accepting the British authorities’ cool aid in recent years, they have now evaporated.

To complete the graphic evidence, we must now observe the dire state of the US Government’s own finances by looking at how its borrowing costs are now soaring out of control.

Clearly the US Government is mired in a debt trap, whereby even if the pace of government spending slows as current debt ceiling negotiations are attempting to achieve, interest expense will drive the US Government deeper into insolvency. It is not a question of if this will happen but simply of when — unless a cohesive argument for significantly lower interest rates can be made.

There are further elements to this debt trap which must be observed. Commercial bank credit is in the early stages of contracting. Without massive monetary expansion by the Fed, mathematically that can only lead to a contracting GDP. The US Government’s mandated welfare costs will increase accordingly and tax revenues will decline. Furthermore, by creating a shortage of available liquidity, contracting bank credit will increase borrowing costs for American businesses and consumers, because banks will demand higher lending margins. And this is something beyond the Fed’s control. Therefore, with the outlook being for even higher interest rates, the cost of US Government borrowing will increase accordingly.

The UK’s debt trap differs in its make-up to that of the US but is no less deadly. Being longer in average maturity the UK government’s debt interest problem may not be so urgently a problem, and relative to GDP total government debt is lower than that of the US. But against these positives, the higher level of the overall yield curve is to be reckoned with.

The next chart shows how total UK government borrowing has increased in recent decades, along with nominal GDP.

The figure for calendar 2022 is now similar to GDP. But GDP also includes government spending, which at 44.6% of the total leaves a private sector base of only 55.4% of GDP to fund government spending. Furthermore, the increase in government debt through its spending has undoubtedly been a major contributor to increasing GDP, masking a stagnating private sector economy.