by Alasdair Macleod, GoldMoney:

In the first part of this report, we highlighted that observed gold prices have significantly detached from our model-predicted prices. While this has happened in the past, prices always converged eventually. However, the delta between the observed and the model predicted price has now reached a record high of around $400/ozt. We thus ask ourselves whether it is reasonable to expect that model-predicted and observed prices will converge again in the future, or, whether we witness a shift in paradigm and the model no longer works.

TRUTH LIVES on at https://sgtreport.tv/

In our view, the only reason for gold prices to sustainably detach from the underlying variables in our gold price model is if central banks (particularly the Fed) lose control over the monetary environment. Thus, it seems that the gold market is now pricing in a significant risk that the Fed can’t get inflation back under control. As we highlighted in Part I of this report (Gold prices reflect a shift in paradigm – Part I, 15 March, 2023), this is happening in the most unlikely of all environments. The Fed has aggressively hiked rates at the fastest pace in over 50 years and it is signaling to the market that it will do whatever it takes to get inflation under control. So why is the gold market still concerned about inflation?

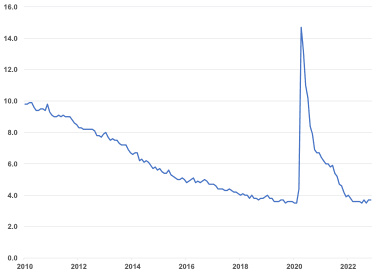

The issue is that so far, it has been easy for the Fed to raise rates sharply to combat inflation. Despite the sharp move in the Fed Funds rate, one may get the impression that nothing has happened yet that would jeopardize the Fed’s ability to raise rates even higher. For starters, the unemployment rate remains stubbornly low (see Exhibit 8).

Exhibit 8: The US unemployment rate remains stubbornly low despite the sharp rate hikes

%

Source: FRED, Goldmoney Research

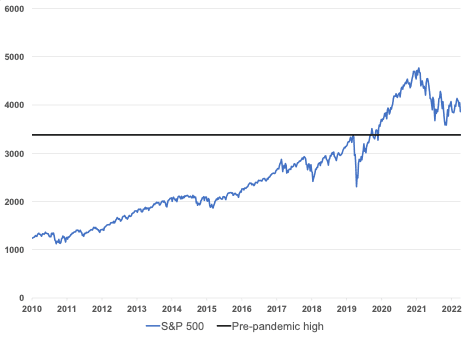

Equity and bond prices have sharply corrected in the early phases of the Fed’s rate hike cycle, but since then equity markets have partially recovered their losses. While equity prices are not the real economy, large downward corrections can impact the real economy nevertheless due to the wealth effect. When people become less wealthy, they spend less, which in turn has an effect on the economy. The impact of this reduction in wealth might also not be meaningful so far as the correction came from extremely inflated levels. The S&P 500, for example, has corrected almost 20% from its peak, but it is still 14% higher than the pre-pandemic highs in 2019 (see Exhibit 9).

Exhibit 9: Even though US equity prices have corrected sharply, they are still well above the pre-pandemic highs….

S&P 500 index

Source: S&P, Goldmoney Research

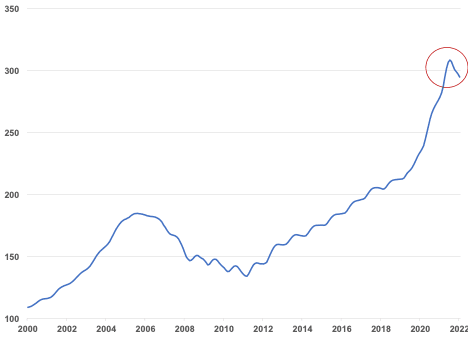

The real estate market has slowed down significantly, but so far prices haven’t crashed (see Exhibit 10), and even though there are a lot of early warning signs, the Fed historically had only become concerned when a crumbling housing market started to affect the banks. While we certainly saw turmoil in the banking sector over the last few days, it was not related to the mortgage business so far.

Exhibit 10: …and home prices – despite the clear rollover – have not crashed yet

Case Shiller US National Home Price Index, NSA

Source: S&P, Goldmoney Research

Hence, at first sight, it appears there is little reason for the gold market to price in a scenario where the Fed loses control over inflation. However, there are plenty of warning signs that things are about to change. In our view, the correction in the equity market is far from over. When the last two bubbles deflated, equities corrected a lot lower for longer (see Exhibit 11).