by Wolf Richter, Wolf Street:

![]() At around 4.75%, plus collateral, these are expensive loans for banks.

At around 4.75%, plus collateral, these are expensive loans for banks.

The Fed’s balance sheet through Wednesday, released today, shows to what extent the Fed has provided emergency loans at around 4.75% interest and against collateral to US banks; and how much it loaned to the FDIC which is tasked with bailing out all depositors at Silicon Valley Bank and at Signature Bank, which collapsed last Friday and over the weekend.

TRUTH LIVES on at https://sgtreport.tv/

At the same time, it shows that the QT-related roll-off of Treasury securities and MBS continued

“Keeping an eye on potential warning signs.”

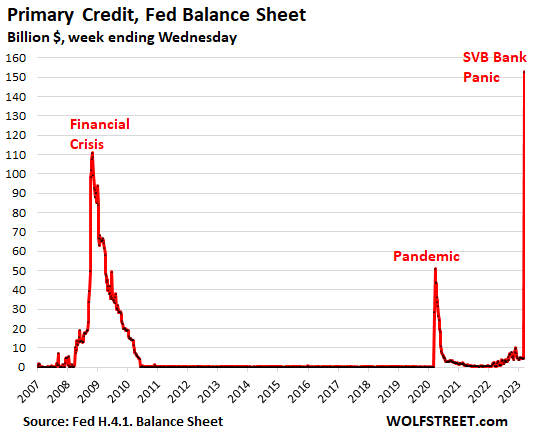

My monthly updates on the Fed’s balance sheet have had for months a section, titled, “Keeping an eye on potential warning signs,” in anticipation of what would happen. And it happened.

The section discussed two accounts on the balance sheet that are unrelated to QT or QE, but are all about whether or not the banks are in trouble: “Primary Credit” (“Discount Window”) for banks in the US, and Central Bank Liquidity Swaps for banks in other countries for dollar liquidity.

On today’s balance sheet, there are two new accounts, the Bank Term Funding Program (BTFP) and “Other credit extensions” that were announced last Sunday as part of the liquidity support for banks and the depositor bailout with the FDIC.

Discount Window: $153 billion. This Primary Credit, as it’s called, allows banks to borrow at 4.75% currently, against collateral. It spiked by $148 billion, from $5 billion a week ago to $153 billion today, the biggest jump in the data.

This is expensive money for banks, and it requires collateral, and so banks won’t borrow long at this rate if they can avoid it, and they tend to pay back those loans quickly, as you can see from the chart below.

They borrowed this way because they needed to have the funds like “right now” when depositors were yanking their money out late last week and this week, as SVB Financial collapsed and panic spread.

But in relationship to the amount of overall deposits, the $153 billion is much smaller than during the financial crisis ($111 billion). In 2008, total deposits amounted to $6.7 trillion; at the beginning of March, total deposits were $17.6 trillion, over 2.6 times the level in 2008.

Bank Term Funding Program (BTFP): $12 billion. The new thingy that the Fed announced on Sunday. Under this program, the banks can borrow for up to one year, at a fixed rate for the term, pegged to the one-year overnight index swap rate plus 10 basis points, currently around 4.6%. Banks have to post collateral, which is valued at par.

But no, banks cannot play cute games with this: To be eligible per term sheet, the collateral has to be “owned by the borrower as of March 12, 2023.” So banks cannot buy securities at market price and post them as collateral at par.

The $148 billion increase in loans at the Discount Window and the $12 billion in BTFP funding amount to $160 billion in new loans that the banks have obtained from the Fed over the past seven days.

“Other credit extensions”: $142 billion. Loans to the new FDIC-owned banks that the FDIC set up to cover all depositors of collapsed Signature Bank and Silicon Valley Bank. The FDIC transferred all assets and deposits of the failed banks into these new banks. And it’s these FDIC-owned banks that borrow at the Fed, and they have to post collateral, while the “FDIC provides repayment guarantees.”