by Jan Nieuwenhuijs, Gainesville Coins:

According to my analysis, the Chinese central bank owned 4,309 tonnes of gold on December 31, 2022, which is more than double than what is officially disclosed. My estimate would make China the second largest gold reserve country after the US. The Chinese private sector holds 23,745 tonnes, bringing the total amount of gold in China to 28,054 tonnes.

China and European countries are in agreement to equalize their ratios of monetary gold relative to GDP in order to prepare for a global gold standard.

TRUTH LIVES on at https://sgtreport.tv/

Introduction

For estimating the true size of the gold reserves of the Chinese central bank (the People’s Bank of China, PBoC), we first need to make a clear distinction between monetary gold (owned by a central bank) and non-monetary gold (owned by the private sector). Without getting into the exact mechanics of the Chinese gold market here, suffice to say that only non-monetary gold imports into China are publicly disclosed. These imports are required to be sold first through the Shanghai Gold Exchange (SGE), and for tax and liquidity reasons virtually all other supply (mine and recycled gold) in China is sold through the SGE as well. On the demand side, private market participants acquire gold at the SGE. It’s unlikely the PBoC buys at the SGE.

Any analysis about the PBoC’s gold reserves based on known import numbers and domestic mine supply is flawed, therefore. It’s true that in the past the PBoC was the primary gold dealer in China—being the monopoly wholesale buyer and seller—but this has changed since the Chinese gold market was liberalized with the launch of the SGE in 2002.

These are the reasons why the PBoC doesn’t buy gold on the SGE:

1. The PBoC wants to diversify its foreign exchange reserves—worth more than $3 trillion at the time of writing—by buying gold mainly with US dollars. Gold on the SGE is exclusively quoted in renminbi: not suitable for the PBoC.

2. As we shall see the PBoC prefers to buy gold covertly. If it buys gold abroad with US dollars, the monetary gold is exempt from being reported in international customs data when crossing borders (non-monetary gold is not exempt). Buying abroad allows the PBoC to purchase and repatriate gold without leaving a trace in the public realm.

3. Gold on the SGE often trades at a premium. The PBoC is more likely to buy gold that is priced lower abroad.

4. In 2015 I was in contact with a precious metals trader at a large Chinese state owned bank. He told me that the PBoC buys gold through Chinese proxy banks, such as the one he worked for, in the global OTC market from bullion banks and refineries in, for example, South Africa and Switzerland. Not at the SGE.

Another person I had the opportunity to converse with in 2015, let’s call him Mister-X, worked at one of the big consultancy firms. He was well connected in the industry. Somewhat similar to my Chinese source, he told to me the PBoC uses proxies to purchase gold in the London OTC gold market.

Early 2017, author and gold commentator Jim Rickards met with three heads of the precious metals departments of large Chinese banks. Rickards stated in the Gold Chronicles podcast published January 17, 2017 (25:00):

What I don’t know is about the Shanghai Gold Exchange sales, they’re pretty transparent, how much of that is private and how much of that is the government [PBoC]. And I was sort of guessing 50/50, 70/30, whatever. What they told me, and these guys are the dealers, it’s 100% private. Meaning, the government operates through completely separate channels. The government does not operate through the Shanghai Gold Exchange. … None of what’s going on on the Shanghai Gold Exchange is going to the People’s Bank of China.

Lastly, in 2014 the President of the SGE Transaction Department said in interview:

The PBoC does not buy gold through the SGE.

Until I bump into evidence convincing me of the opposite, my conclusion is the PBoC doesn’t buy gold on the SGE and thus all known supply in China (import, mine output, recycled gold) must be eliminated from our analysis for estimating the PBoC’s true holdings. Most likely, the PBoC buys gold abroad and from there ships it to vaults in Beijing.

Estimating PBoC Gold Reserves

Let us first have a look at what the PBoC has disclosed in the past.

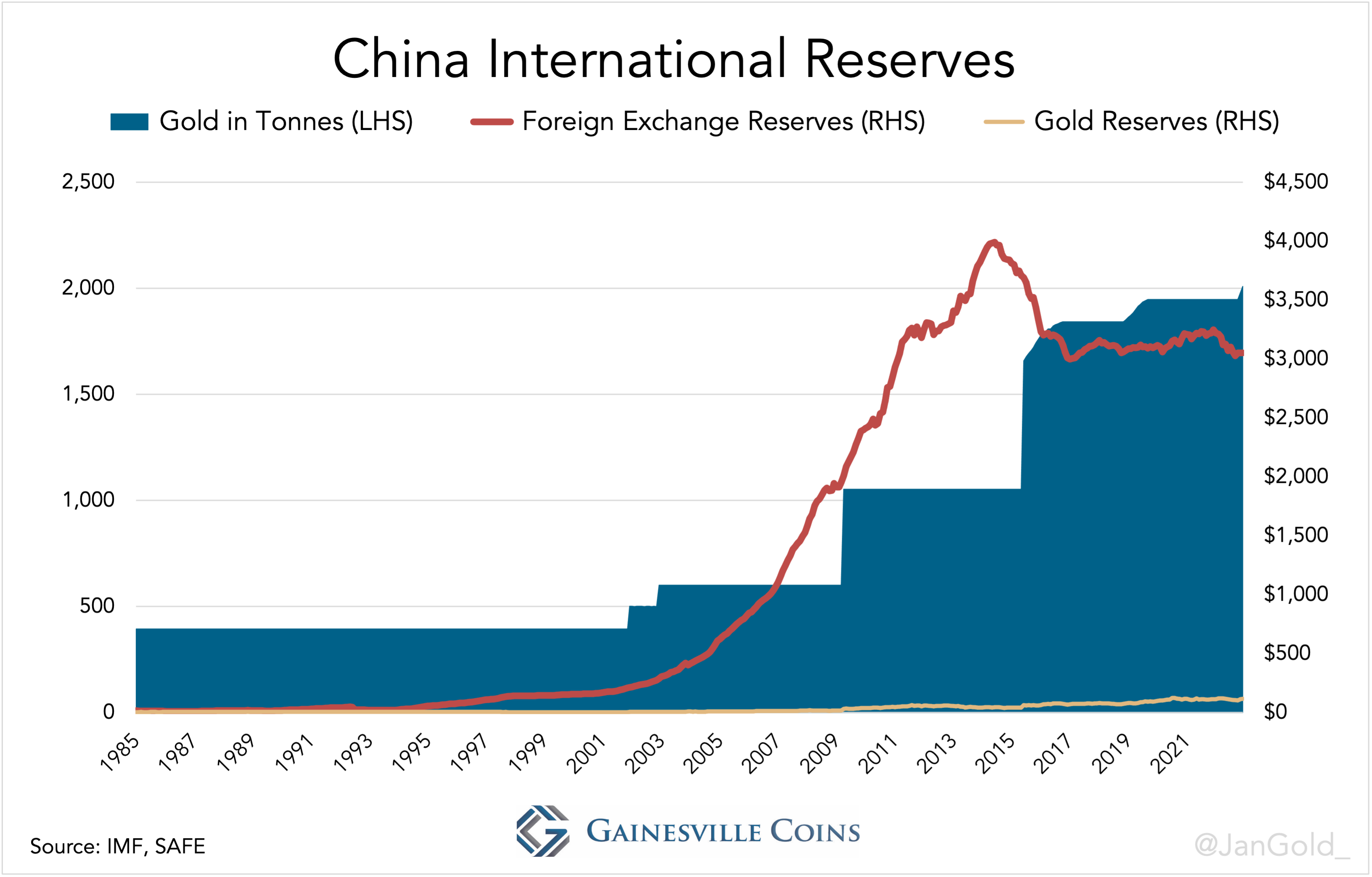

Given China is the second largest economy in the world, it has massive foreign exchange reserves but little gold reserves relative to total reserves, it’s the proverbial elephant in the gold market.

Given China is the second largest economy in the world, it has massive foreign exchange reserves but little gold reserves relative to total reserves, it’s the proverbial elephant in the gold market.

We often see long periods of no purchases and then a sudden large increase in reserves, which suggests they mostly buy by stealth. In June 2015 the Chinese central bank disclosed to have 1,658 tonnes, up from 1,054 tonnes a month prior. Obviously, 604 tonnes weren’t bought in one month.

On one hand the PBoC wants to show the world they are buying gold to catch up with the West, support renminbi internationalization, and move away from the dollar. On the other hand, they don’t want to disclose too much, or they would rock the gold market and drive the price up, which is not in their interest, yet. The Chinese central bank’s interest is to accumulate gold for itself, but it also has a policy of “storing gold among the people” to strengthen China’s economic security (source, page 27). If the price rises, China as a whole can buy less gold.

Read More @ GainesvilleCoins.com